Picture Credit: Unsplashed (Guillaume Perigois)

Empowering SMEs through Accurate Emission Factors

Alexander Pfeiffer (Co-Founder & CEO) // July 2023

The European Green Deal’s Carbon Border Adjustment Mechanism (CBAM) is a ground-breaking initiative aimed at revolutionizing the way the European Union (EU) approaches climate change and sustainability. At the heart of the CBAM lies the crucial aspect of carbon emission reporting for imported goods. This mechanism, designed to curb carbon leakage and incentivize global partners to join the fight against climate change, brings with it both challenges and opportunities for small and medium-sized enterprises (SMEs) in Europe. In this in-depth analysis, we will explore the significance of collecting supplier- and location-specific emission factors for companies that must report on their imported goods. The accuracy of these emission factors holds the key to determining the price these companies will pay for the emissions they import, with even minor errors potentially inflating costs substantially.

The Critical Role of Emission Factors in CBAM Reporting

Emission factors are fundamental tools used to estimate the amount of greenhouse gas emissions associated with a particular activity or process. In the context of CBAM, companies that import goods into the EU are required to report the emissions linked to the production of those goods in their countries of origin. The emission factors utilized in this reporting process directly influence the amount of carbon certificates these companies will need to purchase to compensate for the imported emissions.

Imported quantity x Emission Factor = Imported emissions

170 tons of steel x 2.30 tCO2eq. / ton of steel = 391 tCO2eq.

Supplier- and Location-Specific Factors: Emission factors can vary significantly depending on the energy sources and production methods used in different regions and facilities. Therefore, generic or national-level emission factors might not accurately represent the carbon footprint of a specific product. For instance, a product manufactured in one region with renewable energy may have a lower carbon footprint compared to the same product produced in another region reliant on fossil fuels. SMEs need access to supplier- and location-specific emission factors to ensure they report the actual emissions linked to their imports accurately.

EF for steel produced via BF-BOF route: 2.30 tCO2eq. / ton

EF for steel produced via DRI-EAF route: 2.70 tCO2eq. / ton

EF for steel produced via scrap EAF route: 0.60 tCO2eq. / ton

EF for cleanest 10% steel producers: 0.55 tCO2eq. / ton

Source: World Economic Forum

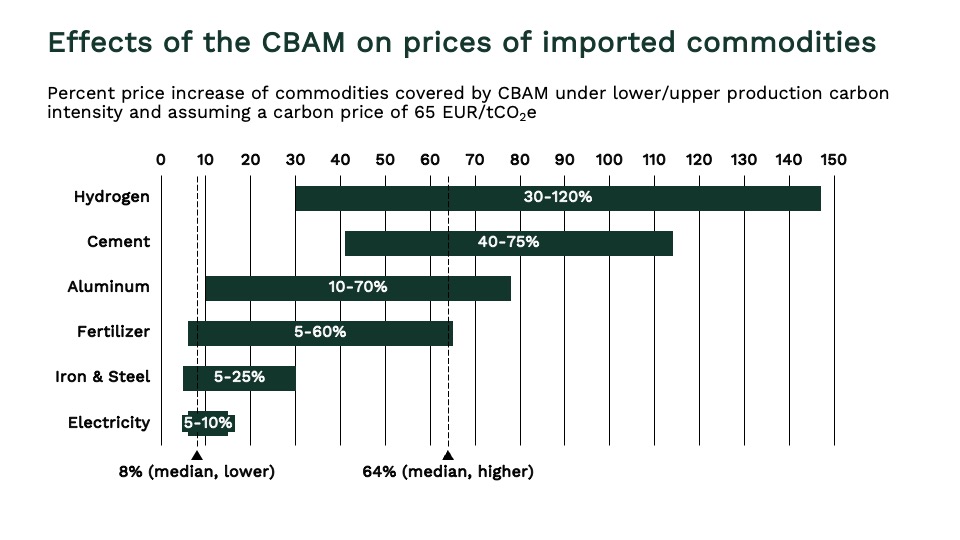

Accurate Reporting to Avoid Financial Impact: For SMEs, many of which operate on slim profit margins, the financial implications of inaccurate reporting cannot be overstated. If the emission factors used for reporting are erroneous or too high, the resulting inflated emission values can lead to an overestimation of required carbon certificates. Consequently, the company will have to pay more than necessary to offset the emissions, directly impacting its bottom line. The difference can be substantial, easily exceeding 8% or more of the cost of imported goods. To remain competitive and financially sustainable, all importers but especially SMEs must strive for precision in their reporting.

Company A imports 170 tons of steel from Supplier B without knowledge of the product-specific emission factor of Supplier B who sits outside the EU.

According to CBAM law the “worst-in-class” EF has to be assumed in this case, e.g., 2.7 tCO2eq. / ton.

170 tons x 2.7 tCO2eq. / ton. = 459 tCO2eq.

Assume that Supplier B uses a clean production route for this steel and the real EF is 0.55 tCO2eq. / ton.

170 tons x 0.55 tCO2eq. / ton = 93.5 tCO2eq.

Imported emissions have been over-estimated by a factor of almost 5x.

From 2026 on Company A must pay for emissions in imported goods (assume a CO2 price of 65 EUR / tCO2eq.)

Company A pays 29,835 EUR (459 tCO2eq. x 65 EUR / tCO2eq.) instead of 6,078 EUR (93.5 tCO2eq. x 65 EUR / tCO2eq.). Per ton this amounts to EUR 175.50 in CO2 price paid instead of 35.75 EUR.

Assume, a ton of steel costs around EUR 700 to import. An additional CO2 tariff of 35.75 EUR would increase this price by 5%, an additional CO2 tariff of 175.50 EUR would increase this price by 25%.

Source: Terralytiq estimations

Encouraging Sustainable Practices: By demanding supplier- and location-specific emission factors, CBAM creates incentives for companies worldwide to adopt greener and more sustainable production practices. When importing companies favor suppliers with lower emission intensities, it encourages global partners to embrace cleaner technologies and processes, thereby reducing the overall carbon footprint of goods traded internationally. The ripple effect of this approach can catalyze a global transition towards more sustainable practices, aligning with the EU’s climate goals.

Challenges in Acquiring Accurate Emission Factors

Despite the potential benefits, obtaining precise supplier- and location-specific emission factors presents various challenges for SMEs. These challenges include:

Data Availability and Transparency: Accessing comprehensive and reliable data on emissions from suppliers in foreign countries can be a daunting task. Diverse reporting standards, lack of transparency, and data accessibility issues in some regions may hinder SMEs’ efforts to obtain accurate emission factors for their imported goods.

Complex Supply Chains: Modern supply chains are often complex and involve multiple intermediaries, making it challenging for SMEs to trace the origin of emissions associated with their imported products. A lack of transparency within the supply chain can lead to uncertainties in calculating emission factors.

Financial and Technical Constraints: Many SMEs might lack the financial resources and technical expertise required to conduct extensive emissions assessments. The cost of third-party audits or emissions calculations can be prohibitive, especially for smaller businesses with limited budgets.

Supply constraints: Today, supply of sustainably produced materials such as green steel or recycled aluminium is limited. Securing access and long-term supply quickly can be a game changer, especially for SMEs who often lack the market power to demand production changes from their suppliers.

Strategies to Overcome Challenges and Enhance Reporting Accuracy

Despite the obstacles, SMEs can employ various strategies to overcome challenges associated with acquiring accurate emission factors for CBAM reporting:

Collaborative Initiatives: SMEs can join forces with industry associations and trade groups to pool resources and collaborate on data collection initiatives. By sharing best practices and collectively funding emissions assessments, these groups can help reduce the individual financial burden on SMEs.

Digital Solutions and Data Sharing Platforms: Digital platforms that promote transparency and data sharing across the supply chain can streamline the process of obtaining supplier-specific emission factors. Blockchain technology, for instance, can facilitate trust and data integrity in emission reporting.

Capacity Building and Support: Governments and regulatory bodies can play a pivotal role in supporting SMEs by offering capacity-building programs and financial incentives. Subsidies or grants for emissions assessments can help SMEs access crucial data for accurate reporting without compromising their financial stability.

Engage Suppliers on Sustainability: SMEs can actively engage their suppliers and encourage them to embrace sustainable practices. By communicating their commitment to environmental responsibility and preferring suppliers with lower emission intensities, SMEs can motivate suppliers to improve their carbon footprint and provide accurate emission data.

Conclusion

As the Carbon Border Adjustment Mechanism (CBAM) takes center stage in the European Green Deal, its requirement for accurate emission reporting on imported goods becomes a critical factor for importers and especially for small and medium-sized enterprises (SMEs). The precision of supplier- and location-specific emission factors is instrumental in determining the cost of carbon certificates that SMEs will need to purchase. Inaccuracies or inflated values in these factors can lead to significant financial burdens, directly impacting the competitiveness and profitability of SMEs. Moreover, the demand for accurate emission factors fosters a transition towards more sustainable practices in the global supply chain.

However, acquiring accurate emission factors presents challenges, ranging from data availability and transparency issues to financial and technical constraints. To overcome these challenges and enhance reporting accuracy, SMEs can collaborate with industry associations, leverage digital solutions and data sharing platforms, and advocate for government support in capacity building and data acquisition.

In embracing the importance of collecting precise emission factors, SMEs have a unique opportunity to play an essential role in advancing the EU’s climate objectives while promoting sustainability in global trade. By navigating the complexities of CBAM and adopting proactive measures, SMEs can emerge as champions of environmental stewardship and contribute significantly to the collective effort to combat climate change and create a greener, more resilient world for future generations.